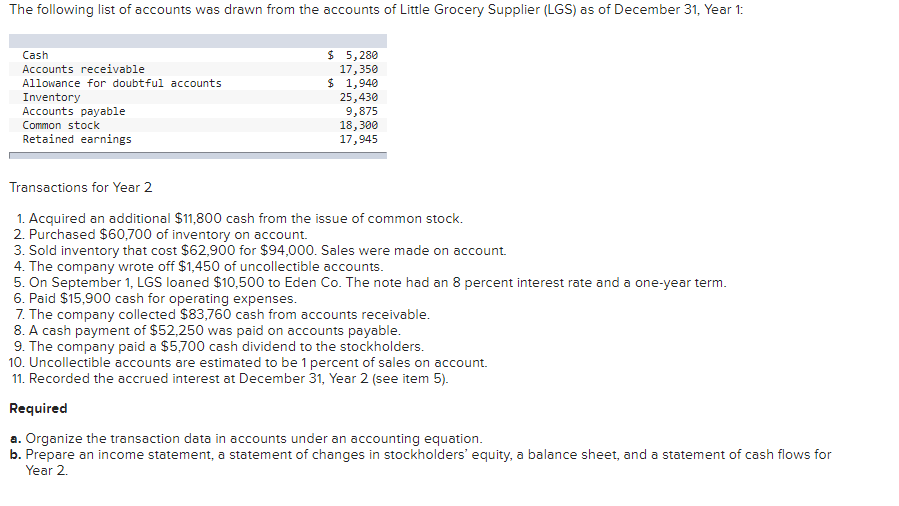

If you’ve been paying in your mortgage for many age, you happen to be given ways to get the most out of the residence’s guarantee. Regardless if you are thinking about a renovation, and make an enormous get, paying off high interest handmade cards, or consolidating most other expenses to evolve the monthly finances, you’ve got choices that individuals is modify on the specific economic desires.

Each other a property security personal line of credit (HELOC) and you may a money-out refinance are often used to supply their residence’s collateral. But what type suits you? Why don’t we compare these two choices:

What exactly is an effective HELOC?

A HELOC is actually a credit line getting flexibility to view fund if needed doing new based credit limit. It makes you improve money whenever you you prefer even more fund. However, you only pay straight back the quantity you owe into the an effective HELOC in monthly installments according to the total count cutting-edge on the borrowing line. As money are manufactured, usage of one part of the loans is available once more so you can advance.

Secret HELOC professionals:

- A lot of time draw months The fresh new mark months toward SECU HELOCs was fifteen many years, which means if you are approved having an effective HELOC using SECU, you really have 15 years to utilize you to credit line to pay for very important programs or requests as they show up.

- Minimum repayments You could always make the minimum requisite payments otherwise shell out even more if you want to reduce the credit line less.

- No costs to have software or credit history With the help of our HELOC, that you do not shell out almost anything to use otherwise undergo a credit check.

What’s an earnings-aside re-finance?

A finances-away refinance allows you to use the security in your home to get into dollars by the replacing your current home loan with a brand new, big loan. Basically, a cash-out refinance substitute your current financial, however, makes your with more currency. Extremely individuals utilize the money it rating of an earnings-out refinance on the a particular purpose otherwise paying almost every other highest expenses.

Having a funds-out re-finance, your supply area of the guarantee of your house doing 90% loan-to-worthy of (LTV) step 1 to possess an initial otherwise second house or more to help you 75% LTV to own a one-equipment money spent. Imagine if your home is worthy of $five-hundred,000. An enthusiastic 80% LTV ratio will mean that you could acquire as much as $400,000.

Secret refinance pros

- Ideal for a massive buy or paying off loans One-time payout out-of a money-away refinance are used for any economic goal your have in mind, whether you need to pay out-of high-appeal credit card debt or another loan, or you are searching for money to cover property repair.

- Potential to replace your credit rating Playing with a cash-aside re-finance to invest down otherwise pay-off a substantial personal debt might help replace your credit score. Lenders look at the complete financial obligation in the place of your available https://paydayloansconnecticut.com/saugatuck/ borrowing from the bank. It is basically expressed due to the fact a share, which they can use to assist determine how better you might be controlling your debt.

- It could lower your interest rate If you are refinancing at the a beneficial date when financial cost features denied because you in the first place funded your own home, an earnings-aside re-finance could reduce steadily the interest on your mortgage repayment.

Selecting the most appropriate solution

A finances-aside re-finance or HELOC is generally what you should meet debt goals, easily pay-off most other debts, or fund huge sales.

When you find yourself still deciding and this loan kind of usually match your greatest, call us in the (877) 589-1547 or visit your regional branch to talk to a lending pro to discuss your options.